Link: https://www.pexels.com/uk-ua/photo/11316617/

If you decide to use your credit card to make your purchase as of last week, you could have to pay an extra cost.

This is due to a long-running legal dispute between Visa and MasterCard being resolved earlier this year, allowing Canadian shops to charge consumers using credit cards as payment.

A class-action lawsuit brought by Canadian firms against the two corporations was settled earlier this year.

As a result, hundreds of millions of dollars in interchange fees the businesses had been paying every time a consumer paid with credit were reimbursed.

Additionally, the settlement permitted them to pass such fees straight on to clients, something they were previously prohibited from doing.

Prior Surcharge Regulations

When a consumer decides to pay with a credit or debit card, a business may tack on a fee known as a surcharge.

Under the Consumer Protection Act of Québec, all-inclusive pricing must be disclosed, with some exceptions for sales taxes (see Section 224 c.). The courts have determined that it is unlawful to impose a surcharge due to this duty.

No other province or territory in Canada, including Québec, has rules that forbid surcharging.

It should be highlighted that while evaluating whether to apply a surcharge, retailers should consider recent modifications to the Competition Act regarding drip pricing.

Offering a good or service at a price that consumers can’t afford because they also have to pay additional taxes or fees makes this practice known as drip pricing. But if necessary, you can use a payday loan Manitoba which will help in a difficult situation.

According to the Competition Act’s civil and criminal prohibitions, this is considered a misleading marketing technique and is forbidden.

However, before Oct. 6, 2022, companies were not permitted to surcharge customers who paid with widely used credit cards because of the usual terms and conditions established by such credit card networks.

Leading credit card networks agreed to change their “No Fee Rule” to allow retailers to levy a surcharge as part of their settlement with the class actions. These Credit Card Network Rules shall go effective as of October 6, 2022, and shall authorize Canadian retailers to surcharge.

Not Every Business Intends to Impose the Charge

A poll of 3,914 Canadian companies performed in September 2022 by the Canadian Federation of Independent Business, or CFIB, found that just 19% of small firms intend to charge consumers a fee for credit card processing.

According to this information, one in five small firms will charge a fee to process customer credit cards.

Since not all companies want to charge for credit card transactions, these fees should be relatively simple to recognize and stay away from as long as they are correctly publicized to customers (which they should be).

But if a company decides to boost pricing instead of levying a processing charge, avoiding the additional expense of using your credit card could be challenging.

According to the CFIB poll, 28% of small firms intend to simply raise their pricing to compensate for the credit card costs.

Telus is one of the significant companies planning first to adopt a 1.5% credit card processing fee. After announcing its plans, the company was bombarded with customer concerns.

The Canadian Radio-television and Telecommunications Commission, responsible for authorizing the fee on Telus’ behalf, has delayed its judgment until early December in response to public outrage.

You must take into account the following information to decide if it is worthwhile to change how your business operates:

- According to Visa and MasterCard, you are permitted to add a premium of up to 2.4% per purchase. MasterCard Debit and Visa Debit cards are not subject to the fee.

- You must notify the consumer at the POI and on the cardholder’s receipt if you intend to impose a premium.

- You must give at least 30 days’ notice to MasterCard and its “acquirer,” the bank or financial institution that handles credit card payments, to impose a fee for MasterCard payments. To do so, complete this online disclosure form and separately tell your acquirer. You just need to give your acquirer a written notification with at least 30 days’ notice for Visa credit cards. Please be aware that most acquirers might still need to prepare to permit surcharging.

- While credit card fees are nothing new, they are unaccustomed to and frequently startle Canadian diners. Although some patrons sympathize with restaurant owners who are still dealing with the repercussions of the epidemic, most patrons may not be pleased to see increases in their bills.

The Future of Credit Card Processing Costs

Over the next several years, the business environment will likely alter as the Canadian government looks for new methods to lower processing and interchange costs.

Although the new regulations are already in place, the actual situation will only alter after some time. While Visa has officially yet to officially announce its latest policy, Mastercard will permit merchants to tack on either the required fee or 2.4% (whichever is smaller).

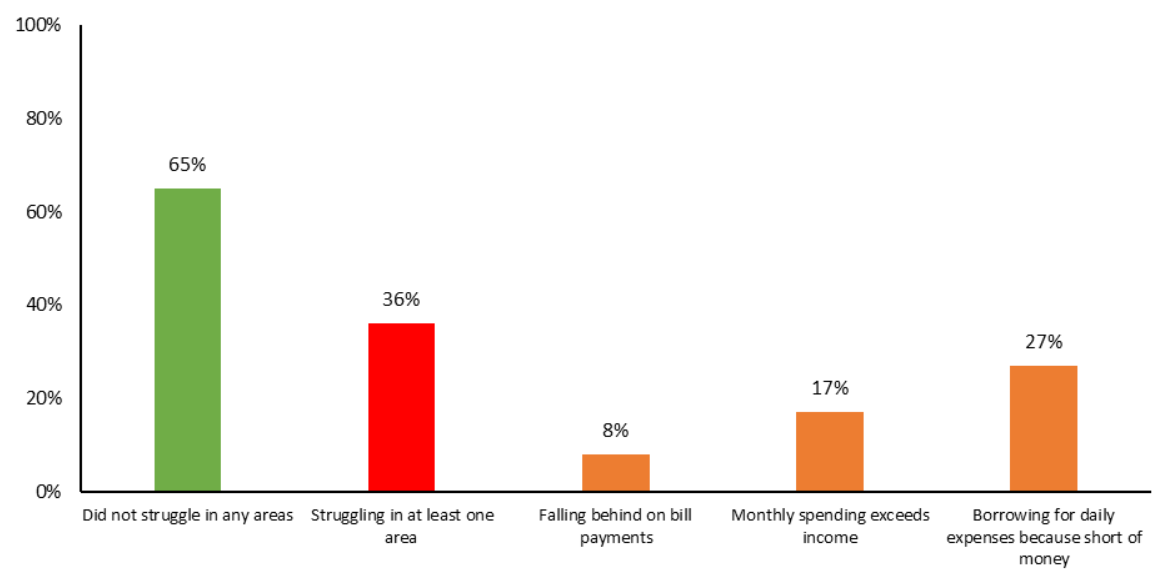

American Express wasn’t named in the case mentioned above. Therefore it is still being determined how they will respond. Over the previous 12 months, 65% of Canadians had no difficulties.

Percentage of Canadians struggling to make bill payments or manage cash flow over the past 12 months

Businesses wishing to take advantage of the law must first register with credit card issuers and notify them 30 days before the levy is implemented.

Furthermore, businesses will only be allowed to charge what they must pay the providers (2.4%).

They will be required to notify clients of the surcharge at the time of payment — by displaying a notice alerting them of the extra and including it on the customer’s receipt.

Furthermore, these regulations will not be implemented in Quebec, where such levies are prohibited under the Consumer Protection Act.

For the time being, there are no penalties for anyone who utilizes cash, debit, or prepaid cards. Although processing and handling costs for various payment methods continue to be passed on to shops, the new tax targets credit cards.

Conclusion

What is the best time to use your credit card moving forward?

The majority of credit cards offer additional valuable perks when making large purchases, such as extended warranties or purchase protection insurance, aside from the apparent advantages of earning cash back or rewards points.

You won’t receive this kind of protection when paying with cash or a debit card. Additionally, a portion of the interchange fee will be covered by your cashback, lessening the pain of the additional charge.

Thomas Jackson is a dynamic and talented content writer at WonderWorldSpace.com, renowned for his engaging and informative articles. Beyond his professional pursuits in writing, Jack is also known for his deep passion for fitness, which not only shapes his lifestyle but also influences his work.